2018 was very special for the Argentine Economy and 2019 looks open-ended

Last 2018 was extreme for the economy: the drought, the vital tariff adjustment, the recategorización to emergent economy, the exchange problems generating a massive devaluation, the large and surprising assistance received from the IMF (merit of this administration however to compensate blunders), double changes of authorities in the Central Bank, the notebooks of the corruption, the presence of the G20, and the hastening of the inflation with a sudden admission into recession.

There is a passage in Ernest Hemingway’s novel The Sun Also Rises (Fiesta in Spanish) in which a character named Mike is asked how he went bankrupt. “Two ways,” he answers. “Gradually, then suddenly.”

Our economic events followed a very similar path. Deep and very positive changes were made outside the economy, but… gradually… very small modifications in awkward macroeconomics and gradualism accumulating actions without results, and… suddenly – as the world and the climate became different – everything collapsed.

The economy is in recession

Against the background of significant vulnerabilities related to persistent imbalances and high foreign-currency debt, a capital flight and a currency run that began in April intensified during August, causing the peso to lose around half of its value this year. As risk premiums rose, financing the large twin deficits became difficult, triggering a large fiscal contraction and recourse to a large IMF programme. Rising interest rates in response to the currency run, as well as faltering confidence, have led to a contraction of investment.

A spike in inflation, lower real wages, and rising unemployment are depressing domestic demand and growth further. An exceptional drought in 2018 reduced exports, exacerbating the large current account deficit.

The search for stability

A combination of massive fiscal and monetary tightening will keep the economy in recession during 2018 and 2019. Private consumption and investment will remain depressed due to lower real incomes and high- interest rates, and unemployment will rise. However, a better harvest and a lower real exchange rate will support stronger exports.

Consequently, the only possible track was to achieve some stability at the expense of a long recession that almost certainly would needle serious problems, something somehow inconvenient during a year of elections, so it might be necessary for the administration completely consume the scarce tools available to keep standing up.

The end of 2018 and the inauguration of 2019 accumulate a strong recession. Industrial activity had a fading of 4% in the year. Due to the new exchange conditions, those operating in the domestic market make certain that the trend will remain negative for at least a quarter of 2019 while those who export expect a stable or growing demand.

Also, construction contracted in the third quarter but since they had a very strongly 2018 the cumulative result was 3% positive.

Wages had an unprecedented reduction in real terms by inflationary acceleration, and retirements to; it can be estimated that they have lost in real terms between 12% and 17% being the retirees the most affected losing 28% of purchasing power.

During the last month of the year 2018, automobile sales suffered an 11% fall.

In the exchange market, after the debacle, January began and continues unwavering with a certain downward trend.

Faster fiscal consolidation and tight monetary policy will be a drag on growth in the short run but are needed to reduce persistent fiscal and current account imbalances. This, and the planned greater independence of the central bank, if implemented, will help to restore confidence.

Foresaw increases in social transfers would cushion the social impact of the recession. In the longer term, reforms in taxes, competition, and administrative procedures will strengthen productivity. Tariffs have fallen in a few sectors, but more is needed to foster integration into the global economy. Reducing barriers to entrepreneurship is also essential.

The country risk fell to its lowest level, until the elections

Concurrently the country risk, after several weeks climbing, fell to 698 points something that was not happening since December 3. It should be noted that in the last month of the year the country risk reached 840. Since then, the setback was 16.6 percent.

For this administration, the best three weeks have elapsed since the crisis that began in May 2018. Country risk reduction-now below 700 points-is a positive indication only because it points toward that the IMF-installed plan to avoid a default by correcting the primary and balance-of-payments deficit is providing the inevitable results, for the time being, the necessary ones. The new monetary regime is working well. The reference rate has been handled prudently, has been stable, and interest rates have begun to fall.

Nevertheless, the country risk is unlikely to fall below 650 since that level indicates to the potential investors in Argentine bonds that the economy is far from having reached the reasonable expectation of being able to cancel its obligations on time and paying the Interests. In fact, that number 700 indicates that our economy should pay 7% above the U.S. Treasury bond rate, i.e. more than 10% annually in the contingency of negotiating a renewal.

What is the reason why country risk will remain at these levels: political uncertainty.

The walking out of this administration mean the entry of a new populism that, by moderate than intended to appear, is not a reliable option for foreign investors, the only source of funding for the next years. Also, the possibility of the return of the kleptocracy continues. As the election process progresses and trends are marked through appraisals, the country risk figure will rise or remain, but will not decline.

Another reason why it will maintain that level is that in order to repay the debt, there is a need for a fiscal and commercial surplus, something quite obvious and elementary. All numbers indicate that there will not be enough growth in 2019 and – if this administration is maintained and adjusted to the fund’s plan – and only 2021 would have a joint surplus adequate to meet the obligations without the need of renewals.

The economy is having two consecutive years of recession, 2018 and 2019, and the results of this last year will be influenced by the forced emergency economic policy. If the fiscal adjustment of 2.5 points of the product had not been necessary, the economy would have grown and the country risk would not be that. In other words, investor confidence would be better.

There may be a quick, however belated recovery for this administration.

The recession is deeper than expected, but it is possible to watch a recovery more rapidly than expected. The contraction was extra acute than predicted in the 3rd trimester, and that makes the growth forecasts for 2018 negative-2.0%. However, with improvements for 2019, the overall activity may be higher than that of 2018 due to weight stabilization based upon the new monetary policy framework.

The elections will imply noise, but policy continuity is the most likely outcome.

Delivering on the fiscal front will be key. With limited market access and a still high stock of short-term debt, access to IMF financing will be of great importance for Argentina. FX stability is key for inflation to continue falling.

Why late?

Due to incapacity or policy errors, this administration did not install this program on either of the two opportunities they had: during December 2015 they chose gradualism that collapsed when operators advocated for the inability of Argentina to face its high indebtedness and later when it got resounding support in the mid-term elections.

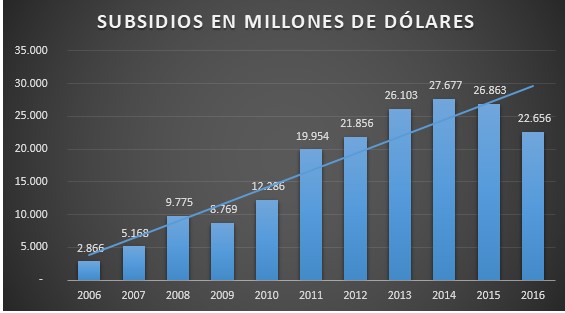

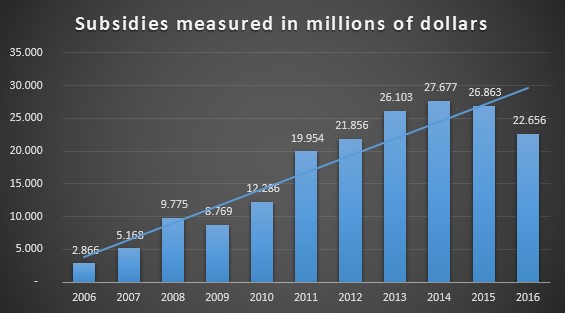

They could have done it if they made comprehend to the population and the markets (by then exalted and receptive) that since 2006 former administration squandered subsidies for the public services (those that even nowadays are all luggage of corruption) and that until the year 2015 the previous administration spent on that issue U $ S 161,318,000,000.

If explained, the need for a tough adjustment would have been understood in order to have normal energy, gas, and transport again. The amount of the subsidies is equivalent in today’s currency, to the entire U.S. subsidy to the countries that participated in the Second World War. Something very sad for the people in Argentina and their future.

Nevertheless, they did not.

Gradualism was chosen and therefore in a year of presidential elections they will have to face the longest and deepest recessive cycle since 2001 and, as responsible for fiscal policy, they must assume the political cost of the economic situation. The question is whether the administration will be able to stand up in spite of everything.

Now – while the emergency program seems to meet its objectives – the current administration cannot hide that December’s downward inflation was above schedule and that the hardcore of inflation – the so-called core-(which does not register seasonality or punctual adjustments) remained without descent. This indicates that inflation in the coming months will not be less than 2%.

As an aggravating it is reported (and already performed) that during the first semester the tariffs of transport, gas, and light, will be readjusted something that is part of the tuning plan to reach 0 primary deficit, naturally this will also have inflationary impact and – worse – political unrest, since the messianic forces, the left and many common disappointed middle class people orchestrate every Thursday marches of protest.

Lack of political timing

On the other hand, the IMF program is being badly communicated. A fiscal adjustment of the magnitude that was necessary has to be installed in a single coup installing all the measures at the same time, and if need be to negotiate hard in the parliament and pressure the governors that should have been done at the time, not during election eve,. Not revealing the awkward situation when they had the opportunity is reflected now in an inelastic country risk downward.

However, this administration continues to report the necessary late and unpleasant measures one by one, affecting separately and independently to each sector making them feel that they are the only ones being punished.

Transport rates and all energy increases in the first quarter, city halls contributions in all provinces in February, with upsurges over 40% and the sad reality that the retirees lost the income of a whole quarter. From October 2017 to October 2018, the pensions increased 18.6% and a 28.3% per annum with an inflation of 48%. There are 9 million people of whom 6 million contributed, and 3 million receive a pension without having contributed anything, including almost half a million middle-class ladies who do not need it.

Once focused inflation as the main objective, total growth of the monetary base was suspended – abruptly-from 44% to 0% to freeze the base to June 2019. The target is now a balanced primary budget in 2019 and a primary surplus of 1% of GDP in 2020.

This implies a fiscal adjustment of 4% of GDP in 2019-2020. Monetary policy will reduce demand for an uncertain time, but there is no other way to restore confidence and reduce imbalances

Maintaining a floating exchange rate, with interventions limited to situations of extreme volatility, keeps the exchange rate at a more competitive level and supports stronger export performance.

Taking into account the current real exchange rate correction and contractionary economic policy, it is guaranteed that the recession will last at least 4 quarters, starting at 2018 and ending at the beginning of the second quarter of 2019.

Discounting the effect of non-value-added primary export earnings, the product in the second part of 2018 fell 1%. As the cumulative recession is 7%, the product would fall 2.1% in 2018, leaving a drag of 4% for 2019.

The question is whether the potential growth to be achieved will be enough to neutralize it or not, and the most sensible answer is to assume that it does not.

Emerging from the recession will take time

GDP is projected to continue to fall in 2019 and unemployment will rise until 2020. Exports will lead the recovery, but domestic demand will take longer to recover from tight monetary and fiscal policies. Using the fiscal space foreseen in the IMF agreement to spend more on well-targeted social benefits would mitigate the likely increase in unemployment and poverty. Inflation and the current account deficit are projected to decline. Once completed, the adjustment process will leave the economy with more solid macroeconomic fundamentals and reduced vulnerabilities.

The projection is subject to large downside risks. Domestic demand could contract more than projected, given the large size of the needed macroeconomic policy adjustment.

Rising unemployment and a deterioration of social indicators could undermine political support for the adjustment. At the same time, fiscal slippage could cause a further loss in confidence. As 70% of public debt is denominated in foreign currency, the depreciation has raised its domestic currency value relative to GDP. While the currency has been stable in recent weeks, further depreciation cannot be ruled out and would add to public debt risks.